Student loans due next month; borrowers could save

Published 3:01 pm Thursday, September 28, 2023

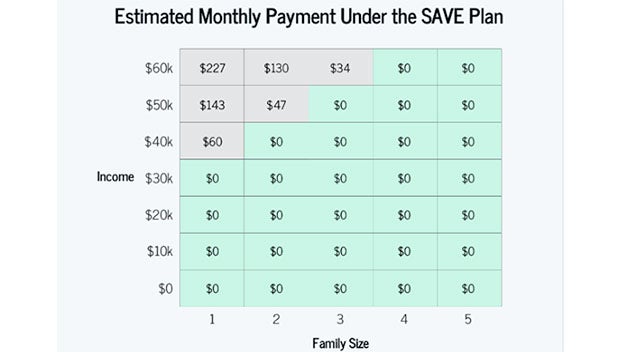

- How much will I pay each month? The SAVE Plan calculates your monthly payment based on income and family size. Starting this summer, if you’re making $32,800 per year or less, roughly 15 dollars per hour, your monthly payment will be $0. If you make more than that, you could save at least $1,000 per year compared to other IDR plans.

|

Getting your Trinity Audio player ready...

|

President Joe Biden’s plan to wipe out $20,000 in student loan debt for millions of bowers may have gotten struck down in June but there is still hope for those struggling to make monthly loan payments.

Millions of borrowers may see a reduction in their monthly student loan payments with a new federal repayment plan.

This option has been made available in anticipation of the resumption of student loan payments in October, following a three-year pause due to the COVID-19 pandemic.

The Biden administration has introduced a plan called SAVE (Saving on a Valuable Education), which considers a borrower’s income and family size when calculating the monthly payments.

According to the U.S. Department of Education, the amount of student loan debt owed is not a factor in this new plan.

While most individuals with federal student loans will meet the eligibility criteria for the new repayment plan, there may be better choices for some. Although the plan reduces monthly payments, it could extend the loan repayment duration, leading to a higher overall cost with accumulated interest.

The SAVE Plan significantly decreases monthly payments by increasing the income exemption from 150% to 225% of the poverty line.

That means you will not owe loan payments if you are a single borrower earning $32,800 or less or a family of four earning $67,500 (amounts are higher in Alaska and Hawaii). Borrowers earning more than these amounts will save at least $1,000 per year compared to the current income-driven repayment plans.

There are other federal student loan programs, called income-driven repayment plans, that also base monthly payments on a borrower’s income and family size. However, low-income borrowers will likely have the smallest monthly payment under SAVE. Additionally, if a borrower makes a total monthly payment, they will not accumulate unpaid interest under the new plan. This means that even if the monthly payment does not cover the accumulated interest for that month, the borrower’s balance will not increase.

The plan eliminates 100% of the remaining interest for both subsidized and unsubsidized loans after a scheduled payment is made.

If you make your monthly payment, your loan balance won’t grow due to unpaid interest.

For example, If $50 in interest accumulates each month and you have a $30 payment, the remaining $20 would not be charged.

The new repayment plan also includes a forgiveness component. Once fully implemented next year, some borrowers may have their remaining balance forgiven after making at least ten years of payments.

To apply for the SAVE plan, borrowers must complete an application for income-driven repayment plans on the Federal Student Aid website.

The SAVE plan and other income-driven repayment plans require a yearly recalculation of payments to account for changes in income or family size.

Typically, if you receive a raise or marry and your spouse has an income, your monthly payment will increase.

However, married borrowers have the option to reduce their monthly payments by filing taxes separately, which excludes their spouse’s income from the calculation.

Borrowers can access the SAVE plan application at https://studentaid.gov/announcements-events/save-plan